Refinance Program for Underwater Homeowners Hits Its Stride

The Obama administration’s Home Affordable Refinance Program is at last helping legions of American homeowners with upside-down mortgages.

The Obama administration’s Home Affordable Refinance Program is at last helping legions of American homeowners with upside-down mortgages.

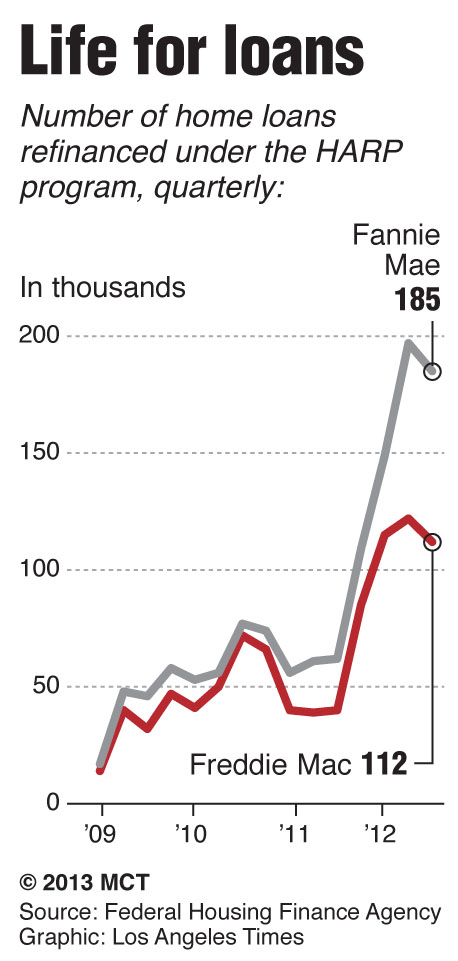

Nearly 1.1 million homeowners with little or no equity were able to refinance last year under HARP, which assists borrowers who are current on their monthly payments. That’s nearly as many as in the three previous years combined, and the latest figures show that early this year, the pace of these refinances abated only slightly.

The program has become a success story after a stumbling start with slack lender participation. Banks were initially reluctant to participate in a program they viewed as risky – refinancing borrowers who owed more than their homes were worth.

HARP is now regarded as a high point in Obama’s mixed record on foreclosure prevention.

“This is a program that has reached a lot of people – probably more underwater homeowners than anybody thought it would,” said Guy Cecala, publisher of Inside Mortgage Finance. “It is also one of the few programs that has rewarded people who have stayed current on their mortgages.”

The program has been successful because it addressed one of the hangover effects from the housing bust: the millions of Americans stranded in expensive, high-interest-rate loans. These borrowers owed too much on their homes and could not refinance. Even the most creditworthy could not get new terms from their lender unless they had 20 percent equity or more.

Obama launched HARP in 2009 as one of two government-backed programs to help underwater borrowers. The better-known Home Affordable Modification Program, or HAMP, encourages lenders to ease loan terms for borrowers who missed payments.

HARP waives the requirement for extensive new underwriting on loans that already are backed by Fannie Mae and Freddie Mac, the giant government-controlled mortgage companies. About 2.4 million refinances have been logged under the program so far.

Initially, the program was underutilized by banks that were worried that Fannie and Freddie might force them to repurchase any new, refinanced loans that went bad. The Obama administration revamped and extended the program in 2011, and it took off last year, as banks found that making those new loans was actually quite profitable.

There remain an estimated 2 million mortgaged homeowners eligible for the program, which has been extended to 2015. But some experts believe the program may have reached its peak potential and may begin reaching fewer and fewer borrowers.

The program does not cover homeowners with mortgages that are in privately held securities. It also allows borrowers to use the program only once, and mortgage rates have fallen from one record low to another.

Congressional Democrats believe the program could be revamped with new laws. Despite several pushes by the Obama administration to promote this legislation, these efforts have stalled inside the Beltway.

Sen. Barbara Boxer, D-Calif., who had introduced legislation that anticipated many of the changes allowed by the Federal Housing Finance Agency, said in a statement that other provisions in her bill would further streamline the HARP process and increase competition.

“I am glad that FHFA has put into place provisions from my legislation that have helped more than 1 million additional Americans refinance their mortgages at lower rates,” Boxer said. “But there is still more to do, and I will work both legislatively and with the administration to remove remaining barriers that have kept responsible homeowners from refinancing.”

Nevertheless, the revamped program has helped borrowers such as Arthur and Dickey Anne Cook, who remain underwater, owing about $270,000 on a Corona, Calif. house that they figure would sell for only $230,000.

The retirees used HARP to get a new loan that knocked nearly 2 percentage points off their interest rate and slashed their monthly payment by $480. By getting rid of the previous home loan, which they obtained five years ago through a mortgage broker, they have now lowered their interest rate to 3.99 percent from 5.75 percent, through HARP.

“We hadn’t missed any payments yet. But in another six months, I probably would have,” said Art Cook, 69, a former phone company manager and Army reservist whose wife taught school. “Things keep getting more expensive, and we’re on a fixed income.”

The way the program works now, refinances are permitted on loans sold to Fannie and Freddie before June 2009. Fannie and Freddie, which back about 60 percent of all mortgages, are already on the hook if the loans go bad, so their risk lessens if the payments are lowered.

Borrowers must owe more than 80 percent of the home value. They can’t have missed a payment for the past six months, and are allowed only one late payment in the last year. And they must have a job or other income to pay the loan, although a full review of employment and tax documents is not required.

To Read The Full Story

Are you already a subscriber?

Click "Sign In" to log in!

Become a Web Subscriber

Click “Subscribe” below to begin the process of becoming a new subscriber.

Become a Print + Web Subscriber

Click “Subscribe” below to begin the process of becoming a new subscriber.

Renew Print + Web Subscription

Click “Renew Subscription” below to begin the process of renewing your subscription.