Rally Ebbs as Investors Seek Safety After Weak Wage Data

Investors made a small move back to safer assets on Friday afternoon after the government’s November jobs report showed continued hiring, but weak wages.

Indexes finished little changed as real estate and household goods companies rose, but banks, which have soared since the presidential election, took losses.

Most stocks finished higher, and the biggest gains went to companies that pay big dividends, similar to bonds. Investors also bought bonds, and prices rose and yields fell.

The dollar also weakened as investors expected less inflation. Thanks to a loss from Goldman Sachs, which closed at a nine-year high on Thursday, the Dow Jones industrial average dipped after closing at a record high a day ago.

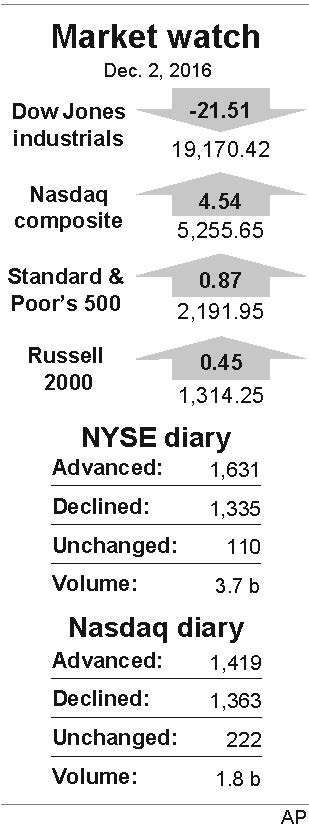

The Dow lost 21.51 points, or 0.1 percent, to 19,170.42. The Standard & Poor’s 500 index rose 0.87 points to 2,191.95. The Nasdaq composite added 4.55 points, or 0.1 percent, to 5,255.65.

The weak finish appeared to mark an end, at least for now, of the post-election rally for U.S. stocks. The S&P 500 and Nasdaq fell this week after a three-week rally took them to record highs. The Dow finished little changed.

The Labor Department said U.S. employers added 178,000 jobs in November as hiring remained steady.

Bond prices, which have been falling sharply since the presidential election, rose. The yield on the 10-year Treasury note fell to 2.30 percent from 2.45 percent.

Lower bond yields pushed investors to buy utility and real estate companies and consumer goods makers, which are often compared to bonds because of their big dividend payments. When bond yields fall, those stocks become more appealing to investors seeking income. General Growth Properties rose 62 cents, or 2.5 percent, to $25.46 and Exelon rose 84 cents, or 2.6 percent, to $33.01. PepsiCo climbed $1.57, or 1.6 percent, to $100.60.

The drop in bond yields also affected banks because yields are linked to long-term interest rates. Lower interest rates mean banks can’t make as much money from lending. Goldman Sachs fell $3.27, or 1.4 percent, to $223.36 and Citigroup gave up $1.25, or 2.2 percent, to $56.02.

The financial sector of the S&P 500 is the highest it’s been since 2008, up 13 percent since the presidential election.

Benchmark U.S. crude added 62 cents, or 1.2 percent, to $51.68 a barrel in New York. Brent crude, the standard for pricing international oils, picked up 52 cents, or 1 percent, to $54.46 a barrel in London. The price of oil surged 12 percent this week after OPEC countries agreed to trim the production of oil next year. That was the biggest weekly rise in oil prices since February 2011.

The dollar fell to 113.67 yen. The euro rose to $1.0660 from $1.0645.

Gold rose $8.40 to $1,177.80 an ounce. Silver jumped 33 cents, or 2 percent, to $16.83 an ounce. Copper lost 2 cents to $2.63 a pound.

In other energy trading, wholesale gasoline picked up 1 cent to $1.56 a gallon. Heating oil added 1 cent to $1.66 a gallon. Natural gas lost 7 cents, or 2 percent, to $3.44 per 1,000 cubic feet.

The CAC-40 in France fell 0.7 percent and the FTSE 100 index in Britain finished 0.3 percent lower. Germany’s DAX fell 0.2 percent. The Nikkei 225 index in Japan shed 0.5 percent and South Korea’s Kospi lost 0.7 percent. Hong Kong’s Hang Seng retreated 1.4 percent.

To Read The Full Story

Are you already a subscriber?

Click "Sign In" to log in!

Become a Web Subscriber

Click “Subscribe” below to begin the process of becoming a new subscriber.

Become a Print + Web Subscriber

Click “Subscribe” below to begin the process of becoming a new subscriber.

Renew Print + Web Subscription

Click “Renew Subscription” below to begin the process of renewing your subscription.